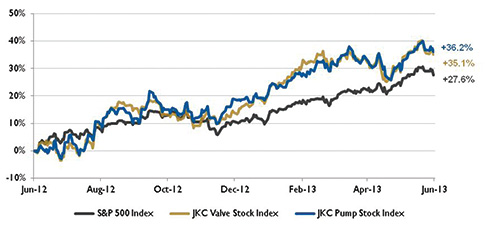

The Jordan, Knauff & Company (JKC) Valve Stock Index was up 35.1 percent during the last 12 months, above the broader S&P 500 Index which was up 27.6 percent. The JKC Pump Stock Index was up 36.2 percent for the same time period.1

Figure 1. Stock indices from June 1, 2012, to May 31, 2013

Source: Capital IQ and JKC research. Local currency converted to USD using historical spot rates. The JKC Pump and Valve Stock Indices include a select list of publicly-traded companies involved in the pump and valve industries weighted by market capitalization.

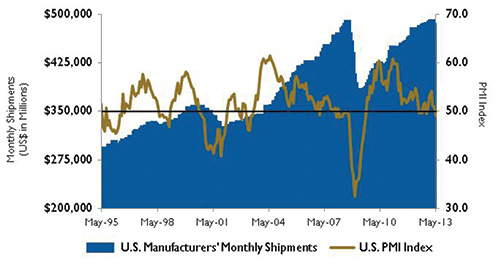

In May, the Institute for Supply Management’s Purchasing Managers’ Index (PMI) fell to 49 percent, a decrease of 1.7 percent from April. This is the lowest PMI reading since June 2009 when it registered 45.8 percent and indicates contraction in manufacturing for the first time since November 2012. The Prices Index has decreased by 12 percentage points since February, registering 49.5 percent in May, representing a drop in overall raw materials prices.

The Bureau of Economic Analysis revised its first quarter 2013 gross domestic product (GDP) estimate to 2.4 percent from 2.5 percent. Strengths in the economy included consumer and business spending, which together added 3.5 percentage points. Gross private domestic investment increased 9 percent from the previous quarter with inventory replenishment, the housing sector, and investments in equipment and software adding the most to this increase. Personal consumption increased 3.4 percent during the last quarter. Weaknesses were in government spending and net exports. With tighter budgets and federal spending cuts because of sequestration, government spending cut almost 1 percent from the GDP with defense spending being the largest drag. Government spending is likely to continue to have a negative effect for the near future.

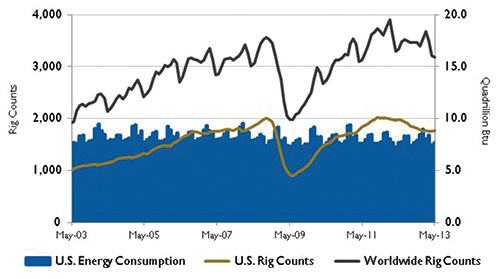

Figure 2. U.S. Energy consumption and rig counts

Source: U.S. Energy Information Administration and Baker Hughes Inc.

Figure 3. U.S. PMI index and manufacturing shipments

Source: Institute for Supply Management Manufacturing Report on Business® and U.S. Census Bureau.

Driven by the rapid pace of tight oil development, the growing supply of domestic light crude oil from the Midwest that usually moves through the Cushing, Okla., market is prompting changes to midstream and downstream infrastructure. Pipelines once used to carry imported oil from Gulf Coast ports to Midwest refiners have been reversed and move crude oil to the Gulf, and their capacity is being dramatically expanded. New pipelines are also under construction, including the southern portion of the Keystone XL project. There have also been major developments in rail transport, in which shipments of crude increased dramatically in 2012. Rail is generally more costly than pipelines for crude oil transport, but unit train loading and unloading facilities, which can often be built quickly, can help narrow the gap between rail and pipeline shipment costs.

The Dow Jones Industrial average gained 1.9 percent in May. The S&P 500 Index gained 2.1 percent, while the NASDAQ Composite was up 3.8 percent. Following signs that the Federal Reserve’s bond purchasing program might slow down or end soon, the market experienced some volatility at the end of May as this bond buying has been a driver of the stock market rally since the beginning of 2013. P&S

Reference

1 The S&P Return figures are provided by Capital IQ.